A vehicle crash took place on a key commuter route.

A burst pipe at home.

A stolen phone on the commute back from work.

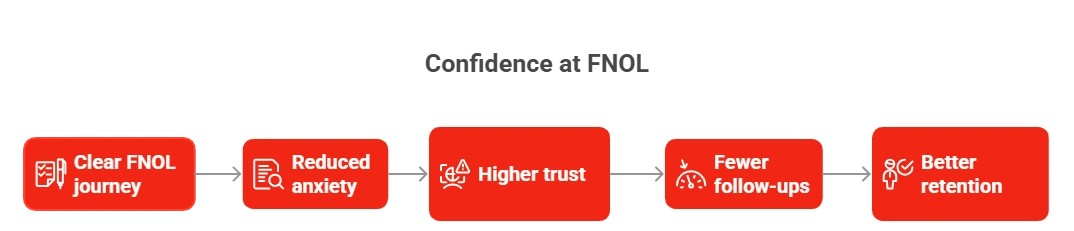

In those moments, customers are not thinking about policies or processes. They are looking for clarity, reassurance, and speed. What they experience next decides whether trust begins, or quietly disappears.

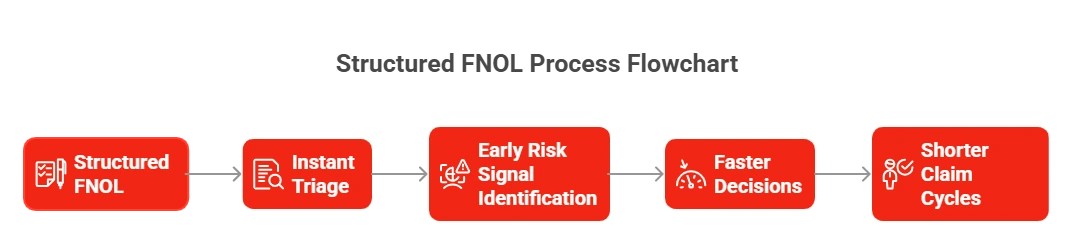

That moment has a name: FNOL, or First Notice of Loss. It is the very first interaction between an insurer and a customer after something has gone wrong. It is where facts are captured, emotions are managed, and expectations are set for the entire claims journey.

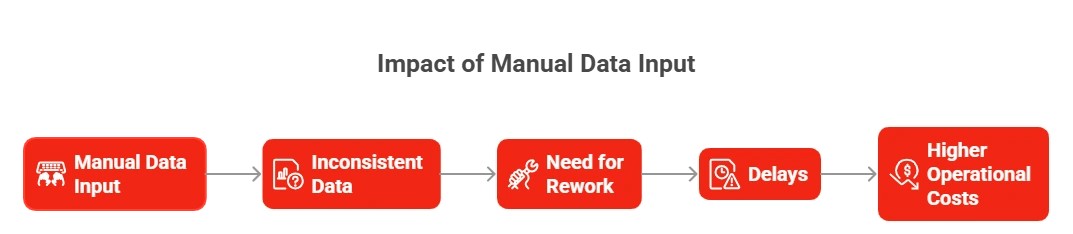

In today’s UK insurance market, shaped by instant digital services and increasing regulatory pressure, FNOL is no longer just an operational step. It is a strategic one. Automation is no longer a “nice to have” tucked away in later stages of claims. It has become a survival strategy, and it almost always starts at FNOL.

This blog explores why automated insurance claims must begin at FNOL, how leading UK insurers are already seeing measurable benefits, and why delaying automation creates unnecessary cost, friction, and risk across the claims lifecycle.

21 mins

21 mins