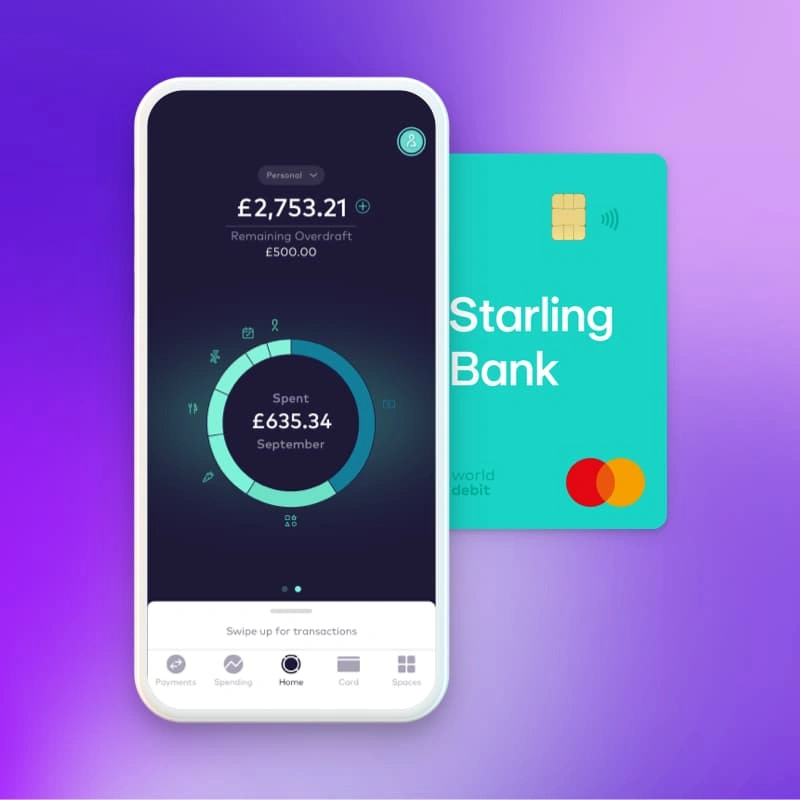

Imagine opening a banking app in the UK today. Within seconds, you check your balance, send money, freeze your card, or apply for a loan, all from your phone.

This seamless experience is exactly why digital-only banks have become so popular across the country. By 2026, nearly 40% of UK adults are expected to have a digital-only bank account, a sharp rise from just 24% in 2023.

→ Challenger banks like Monzo, Revolut, and Starling have transformed everyday banking.

→ Customers expect instant transactions, real-time notifications, and fully digital financial services.

→ But behind these smooth experiences lies a complex layer of financial regulation and compliance.

Digital banks in the UK must operate under strict rules set by regulators such as the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA). They also need to comply with frameworks like AML regulations, PSD2, Open Banking requirements, Consumer Duty, and upcoming regulations like DORA. For a neobank trying to grow from thousands to millions of users, managing these compliance demands manually is extremely difficult.

This is where RegTech (Regulatory Technology) comes in. Today, RegTech is becoming a key part of digital banking infrastructure, helping fintech companies automate compliance, monitor transactions, and build compliance-ready digital banking platforms in the UK while continuing to scale and innovate.

27 mins

27 mins