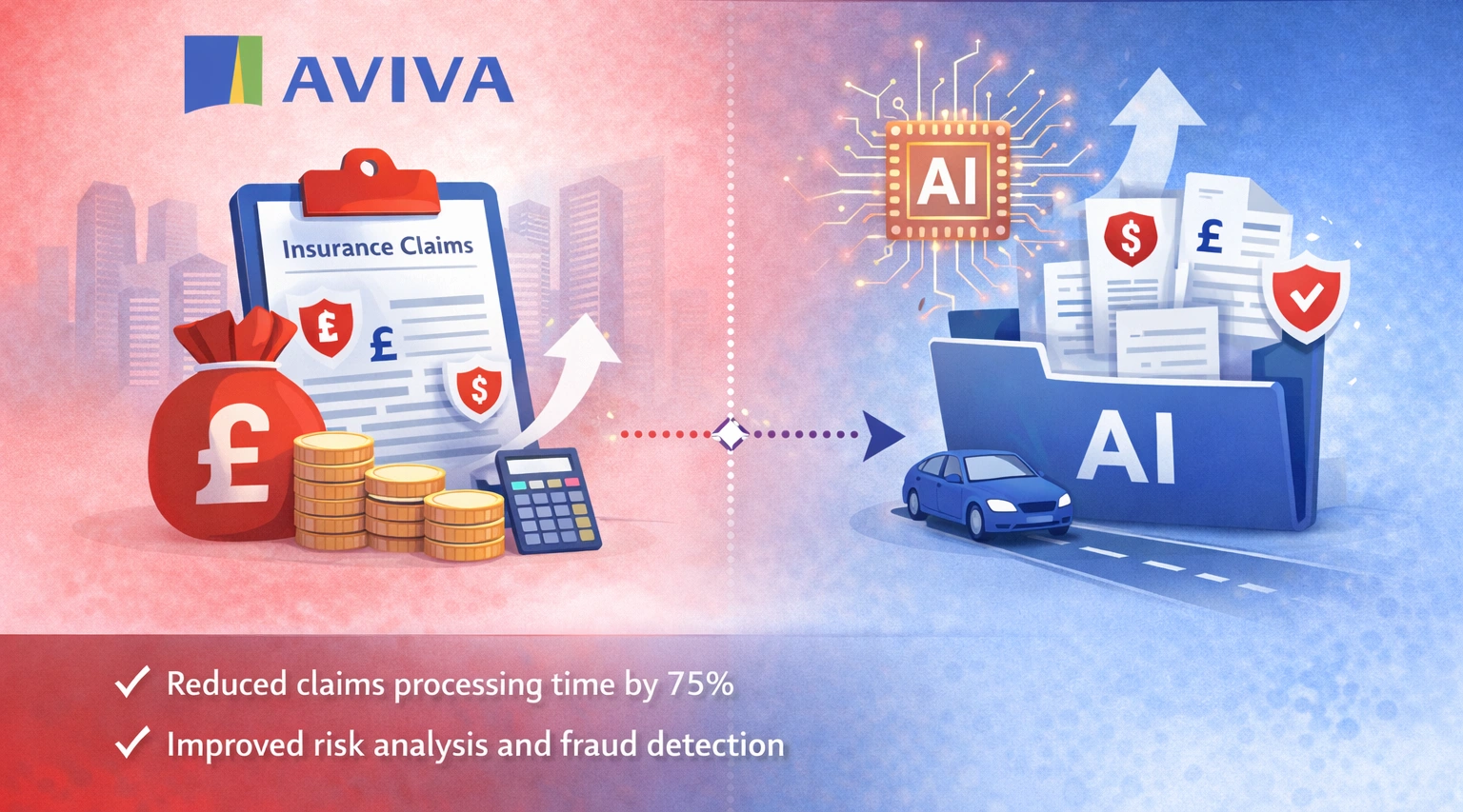

Picture this: it’s 3 PM and your claims team receives 200 FNOL documents: scanned PDFs, mobile photos, broker emails, medical reports. All different formats. All urgent. All needing action today.

This isn’t a rare surge. It’s everyday life for UK insurers operating under rising volume and FCA scrutiny.

Now relax, there is a solution. But first, let’s understand the real gap.

Your OCR system extracts text. It turns images into machine-readable characters. But it does not understand whether a policy is valid, whether a claim breaches limits, or whether risk data is hidden in free text. So your teams still manually check, validate and re-key. Industry research shows insurance professionals spend nearly 30% of their time on repetitive admin work, with manual data entry introducing around 10 errors per 1,000 fields.

21 mins

21 mins