16 mins

16 mins

Feb 06, 2026

A typical day in insurance looks like this: hundreds of documents arrive: PDFs, images, emails, reports. All different formats. All urgent.

This is not an exception. It is daily reality for UK insurers.

Now, here is the real problem.

OCR insurance systems extract text from documents. They convert images into readable data. But they do not understand meaning.

They cannot check if a policy is valid.

They cannot detect risk in free text.

They cannot make decisions.

So teams still review, validate, and re-enter data manually.

This is where IDP vs OCR in insurance becomes important.

Manual effort remains high, errors increase, and time is lost.

In fact, insurance teams spend around 30% of their time on repetitive tasks, with frequent data entry errors.

The gap is clear:

→ OCR extracts

→ IDP insurance understands and processes

| Text Extraction | ✔ Converts image to text | ✔ Converts image to text |

| Context Understanding | ✘ No semantic understanding | ✔ Understands document meaning |

| Document Classification | ✘ Manual | ✔ AI-driven classification |

| Validation & Business Rules | ✘ Not built-in | ✔ Automated validation |

| Fraud & Anomaly Detection | ✘ Not supported | ✔ ML-based detection |

The difference is not cosmetic. OCR reads documents. Intelligent Document Processing interprets them, validates them, and feeds decision-ready data into your insurance systems. In a UK market shaped by FCA oversight, Consumer Duty obligations and rising operational pressure, that distinction directly affects speed, compliance and profitability.

Now let’s go deeper, technically, operationally and strategically, into what separates OCR from Intelligent Document Processing and why it matters for insurers.

For UK insurers, document processing is not a back-office IT function. It directly affects claims cycle time, underwriting accuracy, fraud detection, and FCA compliance.

This is exactly where IDP vs OCR becomes critical, because the real question is not what these technologies do, but what they enable operationally.

Let’s break this down clearly.

Optical Character Recognition (OCR) converts scanned documents, PDFs and images into machine-readable text. In insurance terms, it turns a claim form or broker submission into searchable data.

OCR is effective when:

→ You process high volumes of structured motor or travel claim forms

→ Data fields consistently appear in fixed locations

→ Documents follow predictable, standardised templates

For example, if every motor claim form places “Policy Number” in the top-right corner, OCR extracts that field quickly and reliably.

Operationally, this means:

→ Faster digitisation of incoming documents

→ Reduced basic data-entry workload

→ Lower scanning and indexing overhead

In controlled, structured environments, OCR performs well and delivers measurable efficiency gains.

To understand how this fits into the broader claims journey, explore: Why Automated Insurance Claims Start at FNOL.

However, insurers must understand this clearly: OCR extracts text, it does not understand insurance logic.

It cannot:

→ Validate whether a policy was active on the date of loss

→ Determine whether £5,000 refers to claim value, premium or policy excess

→ Detect repeat-loss patterns hidden in underwriting notes

→ Flag suspicious repair descriptions or anomaly indicators

That means manual validation remains necessary. In high-volume UK claims operations, that manual review layer becomes expensive, slower at scale, and more prone to error.

OCR supports digitisation.

It does not support decision intelligence.

Intelligent Document Processing (IDP insurance) builds on OCR insurance and adds AI-driven intelligence. It combines Machine Learning, Natural Language Processing, and validation engines to classify, extract, verify, and route data automatically.

This is where the difference between IDP vs OCR in insurance becomes clear.

For insurers, this shifts document handling from basic extraction to Claims Processing Automation, where systems not only read data but also act on it.

Intelligent Document Processing changes how insurers move from data extraction to decision automation.

→ Automatic document classification (claim form, medical report, broker submission)

→ Contextual data extraction using Named Entity Recognition (NER)

→ Cross-verification against policy administration systems

→ Exception handling through confidence scoring

→ Fraud and anomaly flagging

→ Straight-through processing for low-risk claims

Where OCR reads: “Previous claim in 2023 for water damage.”

Intelligent Document Processing recognises this as a repeat-loss scenario. It checks internal claims history, evaluates underwriting thresholds, applies risk appetite rules, and routes the case accordingly.

This is not extraction.

This is automated risk interpretation.

For UK insurers, the difference between IDP vs OCR in insurance is not just technical, it is operational.

IDP insurance consistently outperforms OCR insurance because:

→ It understands context, not just text: linking policy data, loss dates and claim values into meaningful insights.

→ It handles unstructured documents: broker emails, medical notes and free-text narratives without template dependency.

→ It validates automatically: checking coverage, policy status and inconsistencies in real time.

→ It flags fraud patterns: identifying repeat claims and anomalies across datasets.

→ It enables straight-through processing: reducing manual intervention and accelerating settlement times.

→ It improves over time: learning from corrections and new document formats.

OCR helps you digitise paperwork. Intelligent Document Processing helps you make insurance decisions faster, safer and at scale.

If you want to see how this plays out across the full claims journey, explore: Automated Insurance Claims Explained: AI, OCR, and Risk Scoring in Action.

For insurers facing FCA scrutiny, cost pressure and digital competition, that advantage is significant.

Insurance fraud isn’t just about numbers; it’s about understanding the full story behind every claim. Traditional systems often miss critical signals hidden in documents, images, and narratives.

— Kognitos, Inc. (@kognitos_inc) February 12, 2026

In our new blog, we explore how AI-driven automation and deterministic logic help…

The FCA’s Consumer Duty isn’t just another compliance checkbox, it’s a fundamental shift in how UK insurers must operate. The Duty requires firms to deliver good outcomes for retail customers, which directly connects to document processing efficiency:

Speed of Service: Slow claims processing fails the “customer support” outcome

Accuracy: Errors in data extraction lead to incorrect pricing, wrong coverage decisions, or delayed claims, all potential breaches

Transparency: You need audit trails showing how customer data flows through your systems

Intelligent Document Processing provides the accuracy, speed, and auditability the Consumer Duty demands. Manual processes and basic OCR simply can’t deliver consistent outcomes at scale.

UK motor repair bills surged 26% year-on-year in Q3 2024, reaching £2 billion. Claims inflation is relentless, and your operational efficiency is the one variable you can control.

Here’s the mathematics: if IDP reduces document processing time from 30 minutes to under 1 minute per document, and your team processes 500 documents daily, that’s saving 242 hours weekly.

At an average salary cost of £35,000 for administrative staff, that translates to roughly £200,000+ in annual labour cost savings, not counting error reduction and faster cycle times.

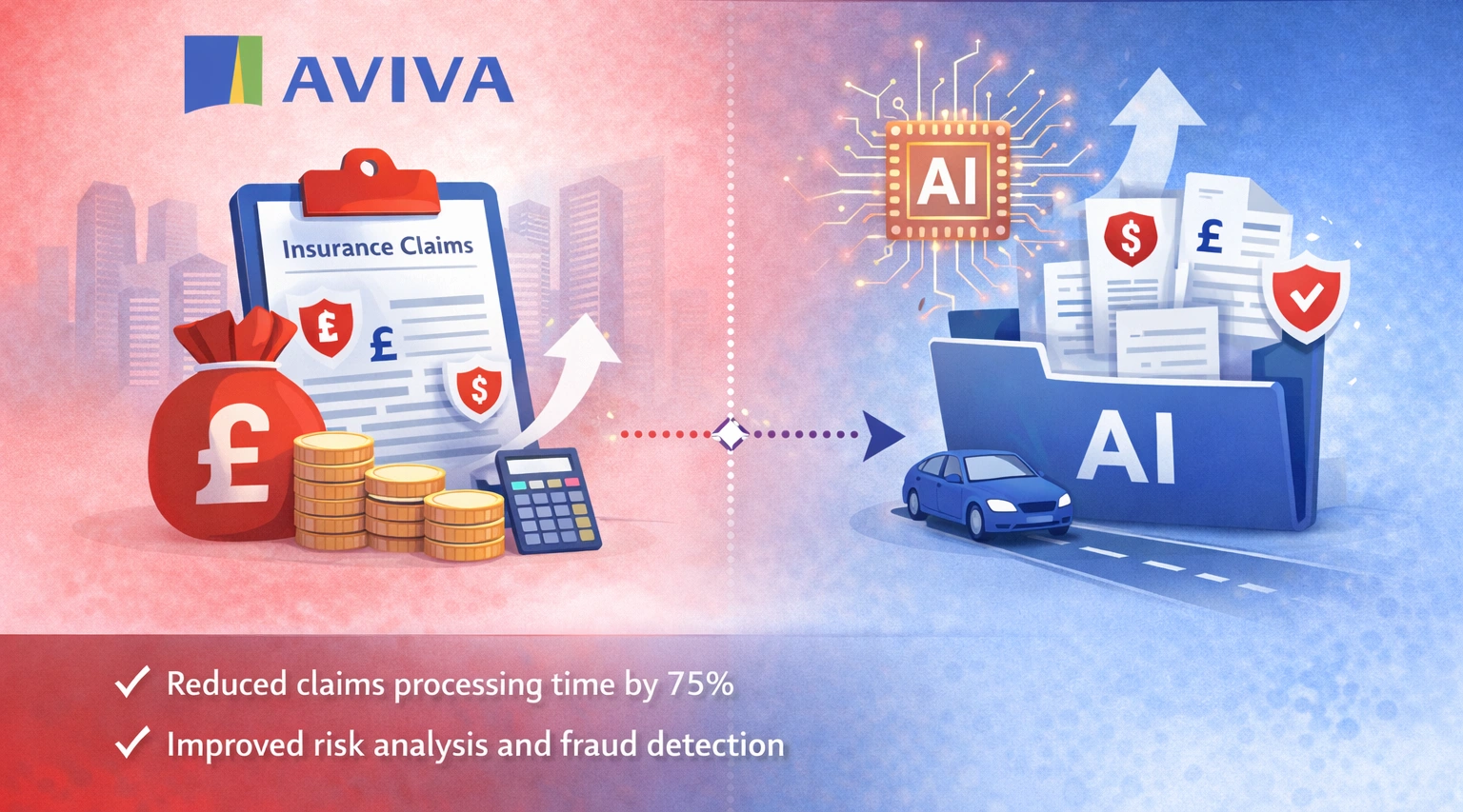

Aviva deployed over 80 AI models across its claims operations in 2024. The impact was significant, liability assessment time reduced by 23 days, claim routing accuracy improved by 30%, and customer complaints dropped by 65%.

They also reported saving over £60 million in motor claims.

This clearly shows the shift in IDP vs OCR in insurance.

Aviva did not rely on basic OCR insurance. It implemented IDP insurance systems that understand context, support decisions, and improve over time.

The message is simple: leading insurers are moving beyond extraction, towards intelligent automation at scale.

The message is clear: the UK’s leading insurers aren’t dabbling in document automation. They’re betting their competitive futures on it.

| Machine Learning Classification | Uses supervised learning models to classify documents based on layout, text patterns and metadata. | Automatically routes FNOL forms, broker submissions and reports to the correct processing workflow. |

| Natural Language Processing (NLP) | Applies Named Entity Recognition (NER) and semantic parsing to extract entities and relationships from unstructured text. | Captures claimant details, loss dates, locations, claim values and incident descriptions from narratives. |

| Computer Vision | Uses deep learning models to detect document structure, tables, signatures, checkboxes and embedded images. | Processes complex insurance documents, repair estimates and damage evidence accurately. |

| Confidence Scoring & Human-in-the-Loop | Generates probability scores for extracted data and triggers review workflows below defined thresholds. | Enables straight-through processing for low-risk claims while controlling decision risk. |

| Agility | Low | High |

Most insurers lose customers not because claims are rejected, but because the experience feels slow, unclear, or impersonal.

FNOL is the most emotionally charged moment in the insurance journey. Automated FNOL delivered through intuitive Customer Experience Portals provides reassurance, clarity, and visibility at exactly the right time. Customers know their claim is logged, what happens next, and when to expect updates.

This early confidence reduces repeat calls, complaints, and churn, while quietly building long-term trust.

OCR remains useful for standardised, high-volume documents where simple digitisation is enough. But modern UK insurance operations deal with varied formats, regulatory pressure and the need for faster decisions, challenges that basic text extraction cannot solve.

Intelligent Document Processing enables insurers to move from reading documents to acting on them. It improves speed, accuracy and compliance while supporting scalable, future-ready operations. For insurers aiming to stay competitive, the shift from OCR to IDP is increasingly becoming a strategic necessity.

OCR converts scanned documents into digital text, while Intelligent Document Processing uses AI to understand, classify, validate and process document data. IDP enables insurers to automate decisions, not just digitise paperwork.

Insurers face complex, unstructured documents, regulatory requirements and the need for faster claims processing. IDP handles document variation, reduces manual review and supports compliance, making it more suitable for modern insurance operations.

Yes. OCR remains effective for high-volume, standardised documents such as fixed-format claim forms. However, it requires manual validation when documents vary or context matters.

IDP automates document classification, extracts key data, validates policy details and enables straight-through processing for low-risk claims, reducing settlement time and operational costs.

When implemented correctly, IDP supports FCA Consumer Duty requirements by providing audit trails, validation checks and transparent processing, helping insurers demonstrate fair outcomes and accuracy.

OCR (Optical Character Recognition): Technology that converts printed or handwritten text from scanned documents, PDFs or images into machine-readable digital text.

Intelligent Document Processing (IDP): An AI-powered solution that classifies, extracts, validates and processes document data using OCR, Machine Learning and Natural Language Processing.

FNOL (First Notice of Loss): The initial notification submitted to an insurer to report a claim event and provide incident details.

NLP (Natural Language Processing): AI technology that enables systems to understand and interpret human language in documents.

NER (Named Entity Recognition): A method within NLP that identifies entities such as names, dates, locations and monetary values in text.

Computer Vision: AI capability that analyses visual elements of documents, including layout, tables, signatures and images.

STP (Straight-Through Processing): Automated processing of claims or transactions without manual intervention.

Human-in-the-Loop: A workflow where AI processes documents but routes uncertain cases to humans for verification.

Confidence Score: A measure indicating how certain the system is about the accuracy of extracted data.

FCA Consumer Duty: UK regulatory framework requiring insurers to deliver fair outcomes, transparency and value to customers.

16 mins